Operator Signal · Before the IC Memo

The Cost of Crowded Markets

Hidden fragilities beneath strong headline growth — the real question is no longer where opportunity lies, but whether underlying economics remain durable as scale, competition, and complexity increase.

|

|

Opening Words

Operator Signal. Before the Investment Committee.

This week’s signals point to a market increasingly shaped by hidden fragilities beneath strong headline growth. Across private credit, AI infrastructure, and corporate transactions, the common challenge is no longer identifying opportunity alone, it is determining whether the underlying economics remain durable as scale, competition, and complexity increase.

As capital continues flowing into crowded markets, traditional indicators of strength can become misleading. In private credit, abundant liquidity and intense competition may be gradually weakening underwriting discipline beneath still-resilient performance. In AI, enthusiasm around model capability is beginning to give way to a more operational question: whether businesses can sustain inference economics once deployment reaches production scale. And in M&A, the Snapple acquisition remains a reminder that even seemingly obvious synergies can destroy value when management misunderstands the operational foundations of a business.

Insights from our network and recent analysis highlight three recurring themes: the risk of excess capital compressing discipline late in the cycle; the growing importance of operational efficiency and cost structure as AI adoption matures; and the danger of underwriting strategic assumptions that appear logical in theory but fail under real-world execution.

The takeaway: focus less on headline growth and more on durability beneath the surface. Pressure-test underwriting discipline during periods of abundant liquidity, evaluate AI businesses through the lens of scalable unit economics rather than model sophistication alone, and treat operational integration assumptions with skepticism when competitive advantages are built on decentralized relationships or unique go-to-market dynamics. In an environment where markets remain crowded but execution windows are narrowing, resilience increasingly belongs to firms that can distinguish structural strength from temporary momentum.

Exact Insight surfaces these patterns early — directly from operator conversations — before they show up in CIMs or IC memos.

Access the Full Briefing →

|

|

|

Insights From the Network

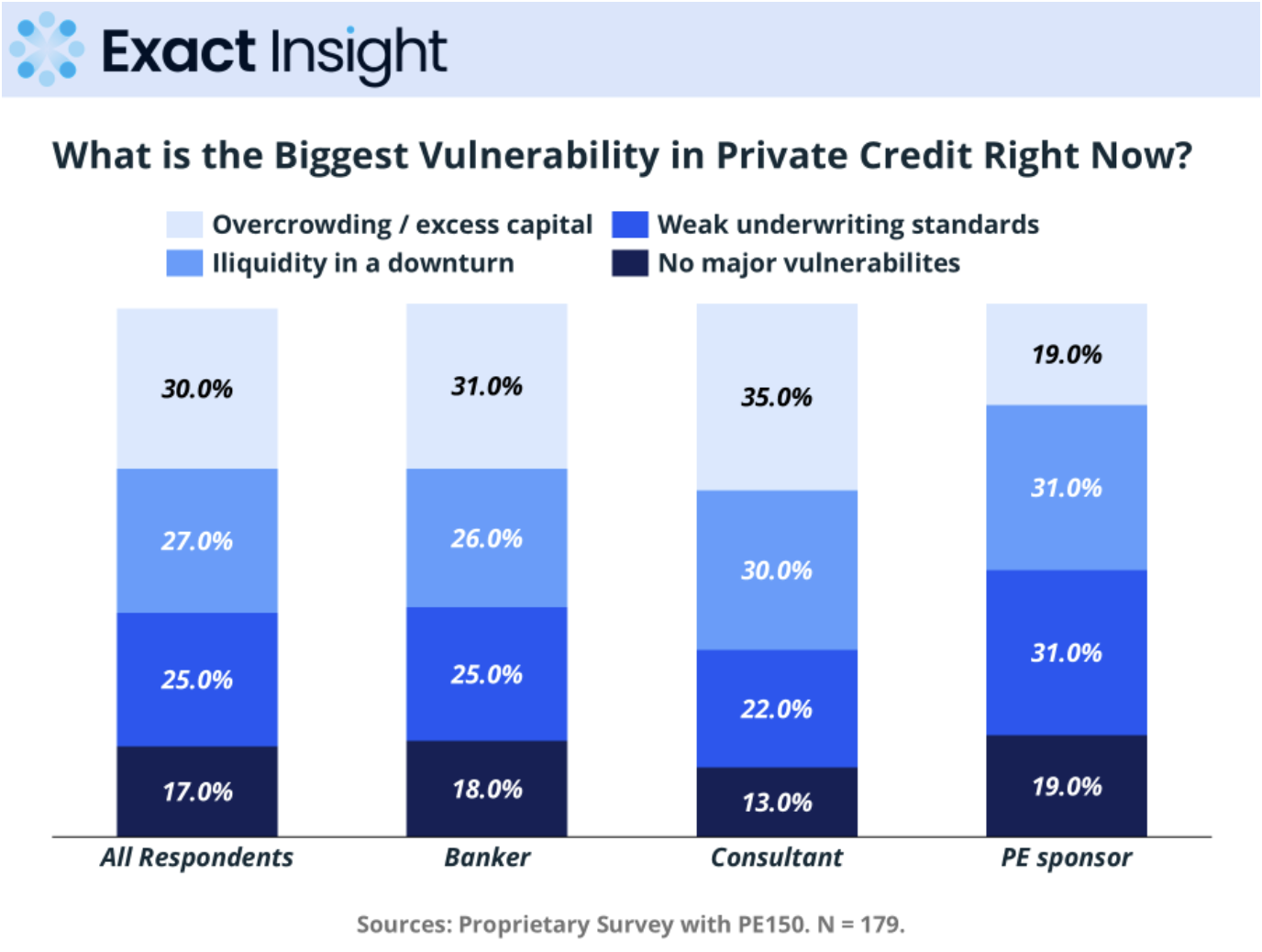

Private Credit: Is Capital Crowding Starting to Weaken Discipline?

Private credit has benefited from a prolonged period of strong fundraising, limited bank competition, and increasing demand for flexible financing solutions. But as capital continues flowing into the asset class, investor concern is increasingly shifting toward underwriting discipline and market crowding.

According to our survey conducted with our partners at PE150, overcrowding and excess capital were identified as the largest vulnerability in private credit by 30% of respondents overall, with consultants expressing the greatest concern at 35%. At the same time, PE sponsors showed materially higher concern around underwriting standards and liquidity risk, both at 31%, suggesting growing divergence between capital providers and market intermediaries on where the real pressure points may emerge.

The key question is becoming: Is private credit still benefiting from structural market opportunity, or are excess capital flows beginning to erode discipline?

Areas that investors should pressure-test include:

- Covenant quality deterioration and documentation flexibility

- Aggressive EBITDA adjustments and sponsor-friendly underwriting

- Liquidity assumptions under stressed refinancing conditions

- Compression in risk-adjusted returns as competition increases

- Exposure to cyclical sectors financed at peak leverage levels

- Dependence on continued fundraising and secondary liquidity

The strongest private credit platforms are likely to be differentiated not by origination volume alone, but by underwriting selectivity, restructuring capability, and the ability to maintain discipline late in the cycle.

Key Insight

Private credit’s greatest risk may not be credit losses alone — but the gradual erosion of underwriting discipline during periods of excess liquidity and intense competition for deals.

Read the Full Article →

|

|

|

Reader Survey

IT Leaders & AI: 2026 State of Practice

We’re surveying IT leaders on how AI is actually being adopted inside organizations in 2026 — what’s working, what’s stalled, and where teams are investing next. Take our 3-minute reader survey and help shape the upcoming report.

Take the Survey →

|

|

|

Deal Autopsy: Lessons from the Field

Snapple: When Synergies Exist Only in the Model

The 1994 acquisition of Snapple by Quaker Oats is widely regarded as one of the clearest examples of how flawed commercial assumptions and misunderstood distribution dynamics can destroy value in M&A.

Quaker purchased Snapple for approximately $1.7bn after the beverage company experienced rapid growth during the early 1990s. Management believed Snapple could be scaled using the same large-scale distribution approach that had successfully expanded Gatorade. Instead, the acquisition quickly deteriorated.

Snapple’s growth had been built through a decentralized network of small independent distributors and strong grassroots brand positioning. Quaker attempted to integrate the business into its centralized mass-retail distribution system, weakening relationships with convenience stores, delis, and independent channels that had been critical to the brand’s success.

At the same time, competitive pressure intensified as larger beverage companies increased investment in ready-to-drink tea and juice categories. Brand momentum slowed, distribution deteriorated, and sales declined materially.

Quaker ultimately sold Snapple to Triarc Companies in 1997 for roughly $300m — representing one of the most significant value destructions in consumer M&A history.

Key Diligence Gaps

- Overestimating transferable distribution synergies

- Misunderstanding the drivers of customer and channel loyalty

- Assuming operational scale would strengthen a brand built on decentralization

- Insufficient consideration of integration risk and cultural fit

- Underestimating competitive response in a rapidly growing category

Operational “synergies” are often most dangerous when they appear obvious. Businesses built on unique distribution models, customer relationships, or brand positioning can lose their competitive advantage when integrated into larger corporate systems.

Read More →

|

|

|

Pre-Deal Intelligence

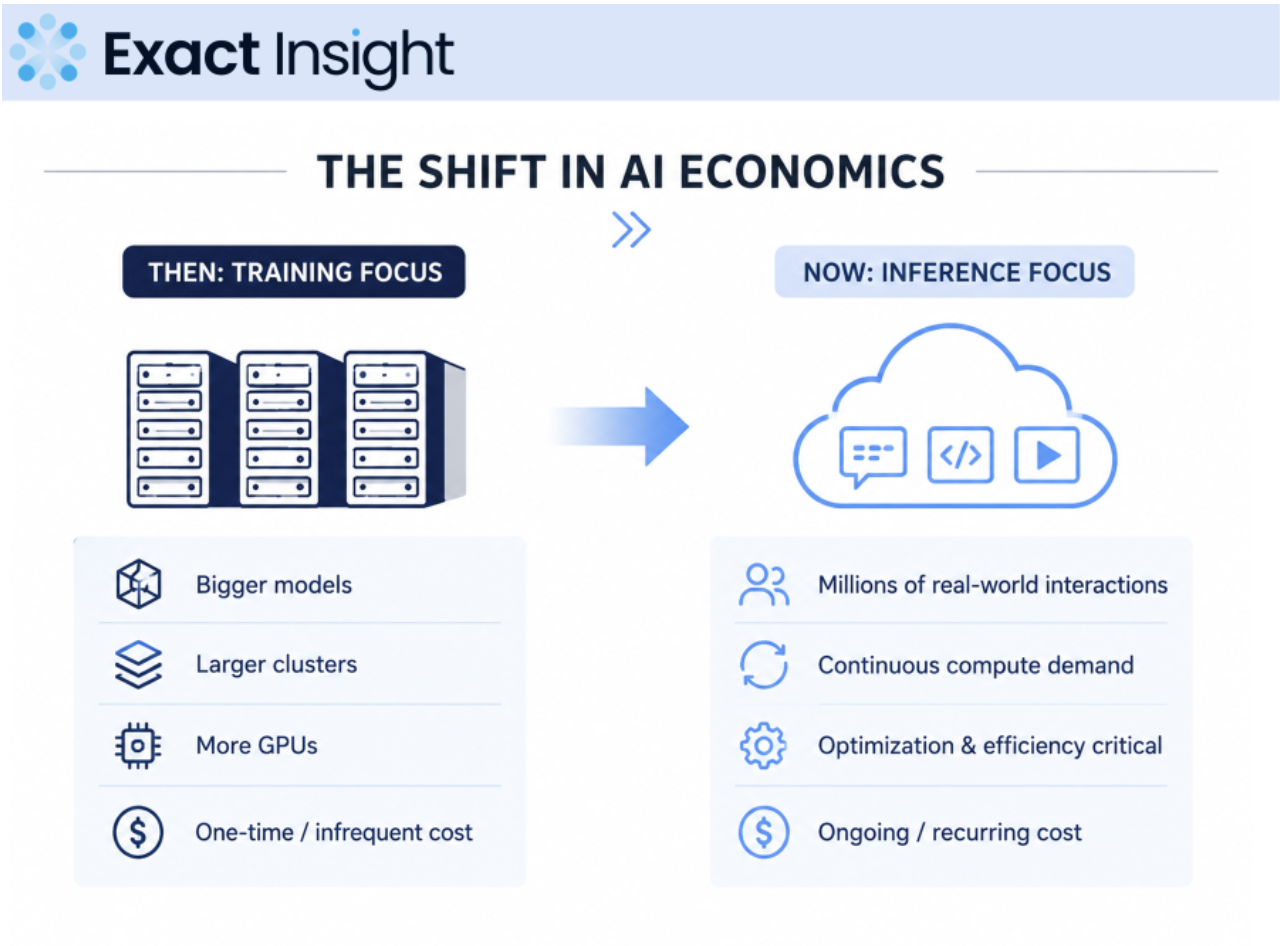

Inference Economics Are Starting to Matter More Than Model Training

For the last two years, AI infrastructure discussions focused almost entirely on training scale, larger models, larger clusters, and greater GPU access. That dynamic is beginning to shift.

As enterprise adoption expands, the real economic pressure is moving downstream toward inference: the ongoing cost of running models in production at scale.

Many AI businesses still appear structurally attractive because usage growth is masking inefficient inference economics. High compute intensity, poor model optimization, and rising energy and networking costs can materially compress margins once deployment scales.

The key question is becoming: Can the business deliver AI economically at production scale — not just train impressive models?

Areas that typically reveal hidden weakness include:

- High inference cost per query or user interaction

- Weak pricing power relative to compute costs

- Heavy dependence on subsidized cloud infrastructure

- Poor workload optimization and low GPU utilization

- Infrastructure bottlenecks around power, cooling, or networking

- Margin sensitivity to rising inference demand

The strongest AI businesses are increasingly differentiated not by raw model performance alone, but by how efficiently they serve inference workloads across millions of real-world interactions.

Key Insight

The next phase of AI competition may be determined less by who can build the largest model, and more by who can operate inference most efficiently at scale.

Read More →

|

|

|

Interesting Articles

Worth a Read This Week

|

|

Want to weigh in on the next survey?

Exact Insight is built from operator signal — and the next cut is already in motion. If you’re a C-suite leader, director, or senior practitioner and want to contribute (and get early access to the findings), join our next survey.

Sign Up to Participate →

|

|